December 6, 2023

Student Loan Debt and

How It May Impact Your Retirement

During the pandemic, federal loan repayments were placed on pause until further notice. Now, three years later, these federal loan repayments have resumed as of October 1, 2023. While the exact impact of the loan payments on Americans’ savings will take some time to measure, this new financial challenge will, no doubt, hinder retirement saving for many. With this in mind, it’s still possible to save for retirement in many cases by just putting a few dollars aside.

According to a Department of Education analysis, the typical undergraduate student with loans now graduates with nearly $25,000 in debt.1 SECURE 2.0 Act retirement legislation tried to address this pressing issue with employer contribution matches for student loan payments, but the actual implementation among most plan sponsors is still far away. With that, only a few companies are considering adopting the 401(k) student loan matching provision from the SECURE 2.0 Act of 2022 because of the potential administrative burden that this provision may impose.

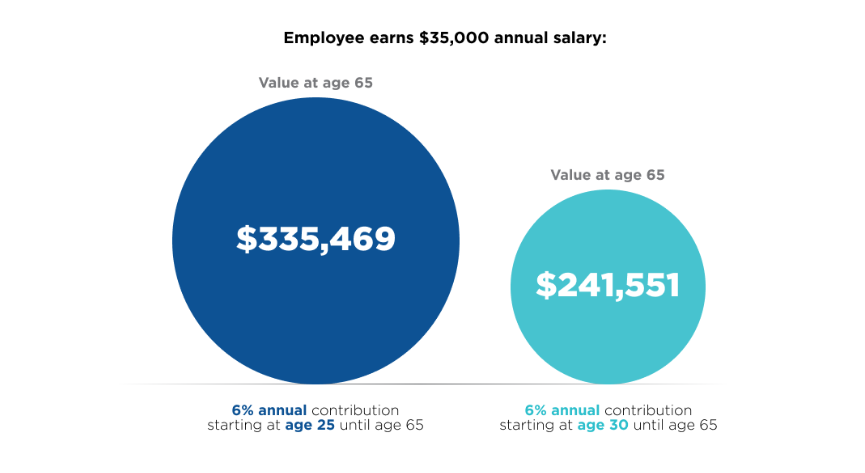

With the student loan dilemma may on the minds of so many people, this is an important time to begin saving if you haven’t already. For example, a 25-year-old with no prior retirement savings who earns a salary of $35,000 and contributes 6% annually to their workplace retirement plan ($2,100 a year, or less than $100 per paycheck) could have $335,469 at age 65, assuming a 6% annual rate of return. But if that 25-year-old waited until age 30 to begin contributing, they would have $241,551—almost $100,000 less in retirement savings—at age 65.

By putting aside just a few dollars each month, you may benefit from the potential growth down the line, making it easier for when you’ve hopefully paid off your student loan debt and are thinking about retiring.

Saving for retirement doesn’t need to be halted while you pay off your student loan debt. You can do both simultaneously by beginning to save in small increments. Overall, the more time your money has to grow, the greater the impact tax-deferred compounding may have on your financial future and retirement.